Mean-reverting

Oct

08

2013

Playing The Bounce - With A Twist

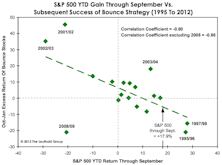

The historical batting average of this strategy has been decent, with gains in 9 of 18 years along with “excess” returns over the S&P 500 in 10 of 18 years. The best Bounce seasons have occurred when the market was either down for the year through September, or up only modestly.

Apr

04

2012

More On Mean Reversion

Could it be possible we’re on the doorstep of another great secular run in stocks? Well… no.

Perception for the Professional

June 2026 Issue

Featured Articles

Sector Navigator

June 2026 Issue