Productivity

Labor Is The Limiting Factor

If the economy slips into recession, the Fed will get all the blame. But it’s worth taking a step back to consider that the die has already been cast: The “capacity” for the U.S. economy to grow is nearly exhausted. Specifically, we’re referring to the capacity available in the labor market.

When There’s No Slack, It’s A Bad Time To Slack Off

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The scene in our neighborhood in the last two summers has become one of relaxed and well-tanned professionals out in their yards overseeing home improvement and landscaping projects. No surprise: Not a single one has told us they’re less productive when working from home!

A New Take On The Labor Market

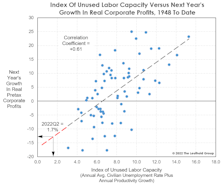

Politicians bemoan the lack of “good-paying jobs,” but what’s the current perspective of employers? According to a simple measure developed by economist Edward Renshaw many decades ago, employers see a lack of “unused labor capacity” in the U.S. that should lead to yet another year of disappointing GDP growth in 2017.

View from the North Country

After years of historical research and endless plotting of productivity trends, our constant vigilance and ceaseless monitoring of vital economic and industrial currents has revealed an amazing correlation. Herein Mr. Leuthold offers his sage wisdom and several solutions to domestic sagging productivity.

“Let’s Get Competitive”: A Conceptual Investment Theme

Capital spending to improve manufacturing and industrial productivity may be much higher than anticipated over the next three years. Management confidence is growing, and attitudes are changing: “Yes, we can compete with our overseas rivals.” Here are the stocks and industries that should be the major beneficiaries of this projected development.

Productivity Plays – A New Look

This conceptual area, even though now widely recognized, still looks attractive. We may soon again be increasing holdings here from current 10% levels. With this issue, we have refined our approach, separating Science & Technology Productivity Plays from Non-Science & Technology. The S&T components may be most attractive. A new index is introduced to track this segment more closely.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue