Sales Growth

Land Of The Rising Stock

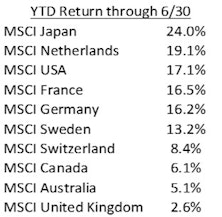

After years of wandering in the wilderness, Japanese stocks are leading the world’s developed markets higher in what has been a robust opening half of the year. The table shows Japan leading the world’s ten largest developed markets (as measured by the MSCI family of international indexes) with a 24% local currency return through June, easily outpacing the pack. Even as the MSCI USA index gained 17% by successfully “fighting the Fed” this year, Japan surged another 7% beyond that outstanding result. We were curious to understand the nature of Japan’s spectacular run in 2023, looking to identify the drivers of this strong and relatively quick jump higher.

Third Quarter 2022 Earnings Waterfall

This earnings season has not been free of concern, and profit margins are clearly weakening from last year’s highs. Our earnings waterfall template highlights several themes coming out of third quarter results.

Discretionary Durables: A Bubble In Fun

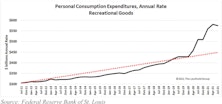

Extremely loose monetary and fiscal policies during the pandemic have created distortions and disequilibria throughout the economy. The most visible bubbles may be in financial markets, evidenced by the boundless valuations applied to visionary startups and the speculative fascination for digital assets of all types. This report examines a bubble of a different kind; not a financial bubble but rather a real-world bubble in “fun”. Producers of recreational goods are flourishing during the pandemic, posting massive sales gains and a tripling of net income, yet selling for miniscule valuations.

Research Preview: Discretionary Durables

While retail spending has boosted staples and durables alike, we believe that discretionary durables have been the prime beneficiary of changing lifestyles and spending patterns, with skyrocketing sales and inventory outages that may not reach equilibrium even in 2022.

Emerging Markets EPS: There's Many A Slip...

If there is one thing sure to make equity investors swoon, it is the prospect of buying into a credible, long-lived secular growth story at a relatively modest valuation. Over the past three decades, Emerging Markets (EM) have proffered just such an opportunity. EM’s economic growth rates have far surpassed those of developed nations, and the valuations attached to EM stocks have often been at a discount to other markets.

However, this combination of secular growth and attractive valuations has not always paid off for investors. The MSCI Index has underperformed the U.S., Europe, and even Japan over the last ten years in local currencies. Furthermore, EPS growth for the EM Index has come in far below its economic growth rate, creating an exasperating drag on Index performance as it tries to keep up with other regions.

Research Preview: Emerging Markets’ Leaky Bucket

Investors view Emerging Markets (EM) as the best source of economic growth across global equity markets, and rightly so. Annualized EM GDP growth of 8.6% since 2001 is more than double that of the U.S. and Europe. However, investors have not captured this extraordinary advance because earnings per share for the MSCI EM Index have lagged far behind EM economic growth rates.

Growth Wherever You Find It

Growth investing is in the midst of a spectacular run this year, extending its decade-long dominance over the Value style. Chart 1 depicts the Growth / Value relationship over the last 25 years through July 31st, with key turning points marked by vertical lines.

Research Preview: Growth, Pure And Simple

Growth investing is in the midst of a record run this year, extending its decade-long dominance over the Value style.

What’s Embedded In The Consensus?

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Market momentum now seems to outweigh simple math in the minds of most investors, and we are not entirely immune. Today our tactical funds are positioned with net equity exposure of 50%, the midpoint of the normal 30-70% range. That’s a higher allocation than if we considered only business cycle dynamics and equity valuations.

Capex Beneficiaries “Delivered,” But Only On Price Action

With optimistic views on capex in late 2017, we built a thematic group of companies that appeared to be potential beneficiaries of higher spending going forward. This group has outperformed the market; but, the capex trend is disappointing and quite concerning.

Once In A Lifetime?

To paraphrase a talking head and the Talking Heads, someday you might find yourself in a beautiful deleveraging, with beautiful valuations, and you may ask yourself, well, how did I get here?

Second Quarter Earnings Waterfall

The S&P 500 reported blockbuster earnings growth again in the second quarter of 2018. With the corporate tax cut boosting profits this year, we were curious to know how much of the improvement was tax driven and how much was due to the exceptionally strong economy.

Perception for the Professional

June 2025 Issue

Featured Articles

Sector Navigator

July 2025 Issue