All Asset No Authority

2022 Asset Allocation Review

We’ve heard for eons that “Low bond yields justify high equity valuations.” Value-conscious investors might have described this conundrum another way: “Low future returns in one asset class justify low future returns in another.” (Mysteriously, only the first rendition became a CNBC catch-phrase.)

“The Streak” Is In Jeopardy…

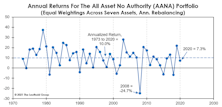

With less than a month to go, our hypothetical All Asset, No Authority (AANA) Portfolio seems likely to beat the S&P 500 on an annual basis for the first time since 2011. However, it’s doubtful that many real-world, institutional multi-asset portfolios were as heavily exposed as AANA to the best-performing assets—commodities and gold.

It’s Been Ugly Across The Board

Aside from a couple specialized approaches, 2022 is shaping up as the second-worst year for “multi-asset” investing since at least 1973. It seems money printing supported more than just the equity subset.

Multi-Asset: Winning By Losing Less

At the beginning of the year, we liked the chances for the “Donut Portfolio” to break its 10-year losing streak against the S&P 500. As a refresher, the Donut holds six of seven key assets in equal weights. The S&P 500 is excluded—a decision probably only suitable for allocators who are self-employed.

Asset Allocation: A Rising Tide Lifts Most Boats

Boy, we thought policymakers had thrown the kitchen sink at the economy in 2020. Evidently, the Fed’s Marriner Eccles building has two kitchens, because they were able to do it again in 2021: M2 grew 13%, the Fed’s balance sheet swelled19%, and the 2021 federal deficit will come in at 12% of GDP.

Time For A “Donut” Break?

Despite a resurgence in Small Cap stocks and Commodities, it still feels like an “S&P 500 World” for asset allocators. The financial media remain obsessed with S&P 500 targets, S&P 500 earnings, and S&P 500 stocks. And why wouldn’t they be?

Liquidity Didn’t Lift Quite Everything In 2020

Last year should have been a perfect one for “diversification” to shine. Extremely high equity valuations entering 2020? Check. A recession-induced bear market? Check. Massive monetary and fiscal stimulus designed to lift all boats? Check and check.

Tough Times For Allocators

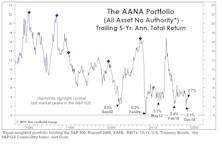

Diversified, multi-asset portfolios have been weak performers for many years. The ultra-flexible, macro hedge-fund manager represents one extreme of the asset allocation continuum. At the other extreme would be the passive holder of multiple asset classes. It’s been a tough three years for this breed, too.

Are You “De-Worsified?”

In recent weeks, we’ve seen the “sell-side” investment community get about as cautious as it ever gets, recommending investors to “trim risky holdings on ‘up’ days” and “stay diversified.” However, these cheerleaders’ idea of diversification is usually to hold more equities in different sizes and styles.

Are You “De-Worsified?”

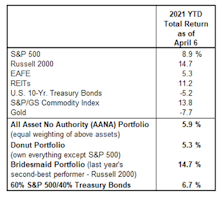

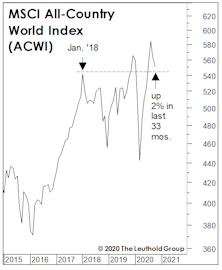

The past 26 months have been wild ones for equity investors, but one could have essentially matched the S&P 500’s healthy return of +18.1% with a portfolio that was evenly split between the “fear” assets of Treasury bonds and gold. REITs have been solid, too, but EAFE and the Russell 2000 are now both total return losers since the beginning of 2018.

A Good Year To “Own It All”

It’s no surprise that U.S. Large Caps were the #1 asset class performer in 2019. We were surprised that last year was the only one of the decade in which the S&P 500 won the annual performance derby. Here we review the annual performance of “Bridesmaid” asset class and sector, “Perfect Foresight,” and Lowest P/E sector.

Odds & Ends

Here are some brief follow-up notes on topics covered in recent months’ Green Books.

AANA: The Good And The Bad

Large Cap U.S. Technology has been the place to be this year, but even an “unmanaged” portfolio with a variety of assets has fared well so far in 2019.

“De-Worsification” Ruled In 2018!

The market difficulties of 2018 were hardly limited to stocks. Commodities, in fact, were the worst performer among the seven major asset classes.

Market Observations

.jpg?fit=fillmax&w=222&bg=FFFFFF)

It’s been one of the worst years on record for diversification, with our hypothetical All Asset No Authority (AANA) portfolio down 7.2% YTD through yesterday. That’s the second-worst year for AANA since 1972, and there’s probably not enough time left for performance to undercut 2008 (-24.9%) for the bottom spot.

Thanksgiving Leftovers

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Whatever one’s preferred leftovers from yesterday’s feast, the odds are good you’ll find them more appetizing than the slop served up by global asset markets this year. Stocks have obviously been turkeys, but all the surrounding trimmings that help diversify a portfolio have proven anything but complementary to the main course.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue