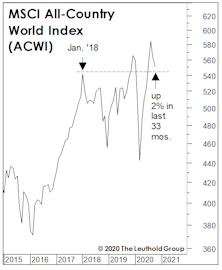

MSCI All Country World Index

4% Club—AAPL Takes On The World

.jpg?fit=fillmax&w=222&bg=FFFFFF)

It’s probably about high time that we check in with our past and present members of the esteemed 4% Club. For those of you not familiar with this vignette: back in the day, achieving a 4% weight in the S&P 500 had been a rare feat, occurring only during periods of extreme enthusiasm for technology, conglomerates or oil. The blessing of membership soon turned into a curse, with most taking just a cup of coffee behind the velvet ropes before being thrown to the curb because of dramatic underperformance to the rest of the Index. Our two most recent inductees seem to be following the proper established Club protocol for not lingering at the party too long. The two other members, however, have been receiving their mail at the Club for quite some time.

Tough Times For Allocators

Diversified, multi-asset portfolios have been weak performers for many years. The ultra-flexible, macro hedge-fund manager represents one extreme of the asset allocation continuum. At the other extreme would be the passive holder of multiple asset classes. It’s been a tough three years for this breed, too.

Ruminations On The Correction

If our market disciplines turn bullish in the weeks ahead, we’ll certainly follow that lead—covering remaining shorts, re-establishing a semi-aggressive market position, and wiping egg off our faces for having called a “cyclical bear market” that slammed the Russell 2000 (-26%), EAFE (-26%), and Emerging Markets (-37%)… but somehow not the one most followed, the S&P 500 (-14%).

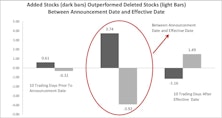

“Index Rebalance Effect” On Stock Performance

Stocks selected for inclusion in the MSCI ACWI have outperformed from the day of the announcement to the day of implementation, while the opposite is true for stocks which are removed. Long-term, however, stocks included in the index do not outperform compared to those that were removed.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue