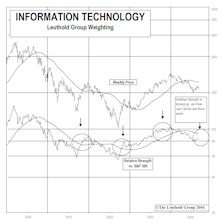

Information Technology

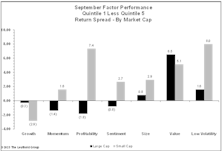

Factor Behavior Differs By Market Cap

Growth has performed much better among large caps than small caps, resulting in higher relative valuations for large caps. Based on factor valuations, we think value provides a more attractive large-cap entry point, while growth looks more attractive within small caps.

Weight Watcher Update—Still Like Value Sectors

While the valuation gap between Growth and Value sectors was compelling just a couple of years ago, it has closed drastically the last twelve months. Our analysis shows that Value sectors (Energy, Industrials) are still more favorable than Growth sectors (IT, Health Care).

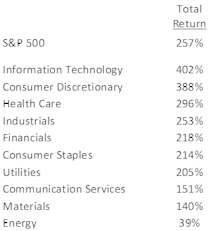

Industry Returns: The Decade’s Winners & Losers

This “decade in review” edition examines the performance of sectors and industries, looking at the best and worst groups to reveal the stories they have to tell.

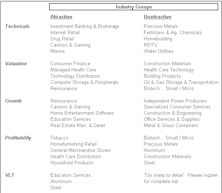

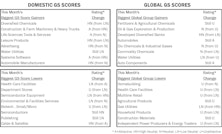

Sector Rankings; Attractive & Unattractively-Rated Industry Groups

The top-three-rated sectors are Communication Services, Information Technology, and Financials. As recently as March, Financials ranked in 9th place out of 11 sectors; it has now placed among the top four since May. Real Estate dropped out of the top three after a two-month visit and is situated in 5th place this round. For the fifth consecutive month, the three lowest-ranked sectors are Utilities, Materials, and Energy.

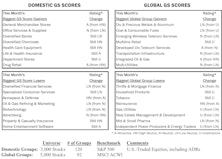

Sector Rankings

The top-three-rated sectors are Information Technology, Real Estate, and Financials.

Information Technology Sector Now Highest Rated

For the first time since late 2017, Information Technology moved into the top-rated spot. This sector has historically produced especially strong results during periods after which it took over the #1 seat.

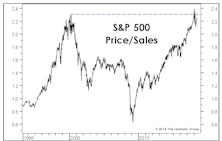

Altitudes Are Too High— And Attitudes Are Getting There

An important feature of this bull market—and a reason for its longevity—is the slow recovery in investor attitudes relative to valuation altitudes...

Two Sector Picks For The Home Stretch

With the Major Trend Index positive and the market about to enter the seasonally most bullish part of the calendar, we’ll offer both a trendy sector and a contrarian one for allocators looking to cap off an already good year. Specifically, we’d recommend heavy exposure to both the Information Technology and Financial sectors, which rate #3 and #1 in the October Group Selection (GS) framework.

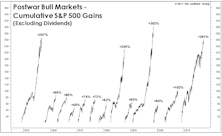

A “Measured” Melt-Up

The stock market “melt up” scenario is underway but has proven less broad than we expected. Just as in the late-1990s, Technology and NASDAQ are the main subjects of investor adulation.

Old School Tech Flies High; Semi Equipment Revisited

Although the glamorous Tech giants have captured investors’ attention of late, from our perspective, the old school, physical Semiconductor plays hold the greatest appeal.

Technology: Popping The “Bubble” Talk

The S&P 500 eclipsed the “Twin Peaks” (2000 and 2007 highs) in 2013, and two years later the NASDAQ topped its 2000 high.

Info Tech, Financials, Health Care—Remain Top Three Rated Sectors

Among the bottom ranked sectors are Utilities, Materials, Energy, and Telecom Services. These four sectors have been the bottom four rated sectors for a minimum of eight months.

Tech In The Pole Position

The S&P 500 Information Technology sector has just broken out to a 15-year relative strength high, and it jumped two spots to the top scoring broad sector position. The breakout in Tech provides a rare example in which foreign market action presaged a major domestic move.

Return Of The Tech? New Group Purchased

Over the past three months the Tech sector has strengthened in our work, as it’s risen back to the #3 position. In line with our disciplines, we increased the Select Industries Portfolio’s Tech exposure via the addition of a new, high-ranking group: Technology Distributors.

Info Tech Sliding

IT’s overall sector rank has been falling recently. Growth has slowed, which has prompted downward earnings revisions, while valuation ratios have remained steady or gotten pricier.

Tech Poised To Outperform!

Our GS Scores currently rank Information Technology as the second highest rated among the ten broad sectors.

U.S. IT Companies’ Global Dominance

A look at U.S. companies’ global IT market dominance, and the key factors that drive the competitive landscape.

“Old Tech” Profiting From Explosion Of “New Tech” Content?

We identify the “Old Tech” players that will likely reap the benefits from the ever-growing volume of data being generated, stored, and transmitted on line.

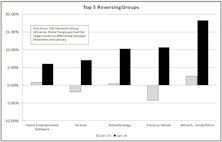

Late March Reversal… And The First Shall Be Last

We examine the impact of March’s strong group leadership reversal on the top and bottom of our group model.

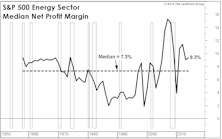

Profit Margins At The Sector Level

All ten of the S&P 500 sectors recorded a sequential increase in four-quarter trailing net profit margins. But consider where sector margins stand today relative to their 25-year medians. Eight of ten S&P 500 sectors are recording profit margins well above their long-term medians.

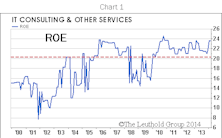

Group Update: IT Consulting & Other Services

We’ve held this group since August 2012. Its GS Score has continued to improve and currently ranks second out of 120 groups. Solid factor readings, coupled with a brightening fundamental picture in both the industry and the sector, keep us invested in this space.

Discrepancies Arise Between December & January

January could be a month that disrupts the current trend, but one month is not enough time to merit a changing of the guard.

There’s A Lot To Like In Systems Software

In addition to impressive factor readings, we like the fundamental trends in this space.

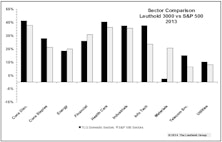

Sector Performance – Finding Discrepancies

Our Tech sector outpaced the S&P 500 Tech sector by 1400 bps and our Materials sector lagged the S&P 500 Materials by 2300 bps. Here’s why…

GS Scores in 2014

Looking forward, groups from the Information Technology, Health Care, Consumer Discretionary, and Financials sectors look appealing.

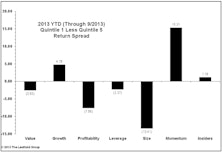

2013 Factor Performance: What Worked? What Will Keep Working?

Momentum and Value worked in 2013. Materials and Financials were the easiest sectors to exploit; Discretionary and Tech the most difficult. Momentum works in December; Value and Small Caps at the start of the year.

Tech Sector Looking Healthy - Technology Distributors Purchased

Our quantitative measures for the group and broad sector continue to improve; we think the recent relative turnaround in these stocks is poised to continue.

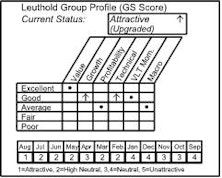

Group Models: Info Tech Tops Domestic, Financials Remain Atop Global

Both models have numerous Information Technology and Financials groups in Attractive territory. Neither model has any Unattractive Tech groups. Alternatively, neither model has any Attractive Utilities groups, while several Utilities rate Unattractive in each.

Group Models: Info Tech Tops Domestic, Financials Tops Global

Both models (particularly domestic) have a number of Attractive rated Information Technology groups and no Unattractive rated Tech groups. Financials’ domination of the Global Attractive range continues.

A Turn In Tech’s Tide?

Technology may be the biggest sector disappointment in the current eight-month leg of the rally, if not for the entire bull run from early 2009.

Electronic Manufacturing Services Purchased In Select Industries

Attractive valuations, improving growth and technical strength are the key drivers. The group offers an opportunity to participate primarily in the overall growth of computing devices.

Group Models Agree On Energy & Materials

But Information Technology rises to the top of the Domestic model, while the trend of Financials domination in the Global model remains intact.

Domestic and Global Group Models: Strong Agreement On Financials

Our Domestic Scores have five Financials groups rating Attractive; these same five industry groups are Attractive in our Global model. In total, seven Financials groups rank Attractive in the Global model, with insurance groups looking particularly Attractive.

Info Tech As The New Leadership Sector?

There has been a lot of talk recently by PMs and market commentators citing Technology as the place to be. However, when the performance is disaggregated, it becomes clear that this broad sector does not in fact look so good. There are pockets of strength (like the Tech…Big Ten), but our message to readers is be careful.

Technology: Seven Years After The Bubble And Still Struggling

- Our quantitative work on technology remains poor, and only a single tech subgroup—Technology Distributors—makes our current Attractive list. Per the Group Selection disciplines, there are currently no technology stocks in our Select Industries portfolio.

- Tech’s underperformance has helped restore better relative value to the sector, but valuations aren’t yet cheap enough for a big “reversion-to-the mean” bet.

Insider Buying/Selling In Technology Sector…..Some Isolated Buy Signals

At the market lows, the Tech insiders while not net buyers clearly slowed their aggressive selling.

Tech Watch Revisited – Examining The Bullish Case For Info Tech

Technology continues to be a hot topic. This month’s “Inside The Stock Market” takes an objective look at the Tech sector.

Sustainable Tech Rally?

Sustainable Tech rally or nothing more than playing catch-up?

Sector Spotlight...on Technology

Looking for Q4 tactical trading opportunities in Tech.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

April 2026 Issue